This article is an update to one from June 1, 2018 titled “Impact on Steel Markets & Products of Trump Administration Trade actions”. You can read that memo here: https://marmacinc.com/impact-on-steel-markets-products-of-trump-administration-trade-actions/

Following U.S. trade policy over the course of the past 18 months has been difficult. Media reports are often speculative, sensational, and sometimes don’t provide the entire story. Interpreting government pronouncements to be bluff, intent, or action is frustrating. For those of us in the steel and construction supply industries, there is little question that trade policy has affected our businesses. This memo is intended as a short summary of the situation and is for informational purposes only. I am not an authority on trade policy or politics nor am I a trade attorney.

An Updated Summary of Tariff Actions

The Trump Administration has acted in three areas using executive authority to impose tariffs on a range of imported products from various countries.

Section 202 Tariffs

In January 2018, President Trump imposed tariffs on solar panels and washing machines, exercising executive authority according to Section 202 of the Trade Act of 1974 [1]. To the best of my knowledge, these tariffs remain in effect as of today.

Section 232 Tariffs

Steel & Aluminum – In March 2018, President Trump imposed tariffs of 25% on certain steel and aluminum imports, exercising his authority according to Section 232 of the Trade Expansion Act of 1962 [2]. Tariffs were imposed on specific countries and targeted mill products – i.e. material produced at the mill or smelter – and didn’t include “downstream” products made from mill products. The Administration has changed rates and target countries since initially imposing Section 232 tariffs. Exemptions have been granted to countries who have negotiated agreements to restrict imports via quotas or other methods. Tariff rates on steel imports from Turkey rose from 25% to 50% and have since returned to 25%. Steel imports from Mexico and Canada were originally targeted with 25% tariff rates but tariffs were lifted in May 2019 [3] after ratification efforts got underway in all three countries for the U.S.-Mexico-Canada Agreement (USMCA). This treaty was signed in November 2018 and is considered a replacement for the North American Free Trade Agreement (NAFTA). The bulk of Section 232 tariffs remain in effect as of today.

Automobiles – In May 2018, US Commerce Department initiated a Section 232 investigation to “…determine whether imports of automobiles… and automotive parts into the United States threaten to impair the national security.” [4] Commerce submitted a report to the President in February 2019 and the President has delayed action on that report while the USTR negotiates with countries referenced in the report. [5]

Section 301 Tariffs

In August 2017, the White House directed the Office of the US Trade Representative (USTR) to consider an investigation of “…China’s laws, policies, practices, or actions that… may be harming American intellectual property rights, innovation, or technology development” under Section 301 of the Trade Act of 1974. [6] The USTR issued the results of its investigation in March 2018 and found that China was conducting unfair trade practices. [7] In response and through the course of on-going negotiations with China, the Administration has imposed Section 301 tariffs in what are now referred to as 4 Lists for affected products.

List 1 – Action was initiated in a Presidential Proclamation on March 22, 2018 and a final list was released on June 15, 2018. [8] List 1 went into effect July 6, 2018 and targeted $34 billion in Chinese imports to the U.S. List 1 rates are scheduled to increase from 25% to to 30% as of October 1, 2019. [9]

List 2 – Action was initiated in the same Presidential Proclamation as List 1. A final version of List 2 was released on August 7, 2018 and went into effect August 23, 2018. [10] This action targeted $16 billion worth of Chinese imports to the U.S. List 2 rates are also scheduled to increase from 25% to 30% as of October 1, 2019.

List 3 – The Administration initiated action on List 3 in June 2018. [11] The final version of List 3 was released on September 18, 2018 and targeted $200 billion of Chinese imports to the U.S. [12] Tariffs on List 3 products went into effect September 24, 2018 and imposed an initial 10% rate that was scheduled to increase to 25% on January 1, 2019. On December 1, 2018, the Administration announced that it would delay the planned increase until the following March and delayed it indefinitely on February 24, 2019. The increase to 25% was finally imposed May 10, 2019. [13] List 3 rates are scheduled to increase to 30% on October 1, 2019. The President announced via Twitter on September 11, 2019 that the increase would be delayed on List 4A until October 15.

List 4 – Action on List 4 was initiated by direction of the President on May 10, 2019 and targeted $300 billion of Chinese imports. A proposed version of the list was released by the USTR on May 17, 2019. [14] The USTR announced on August 13, 2019 that a 10% tariff rate would be imposed on a portion of List 4 (now referred to as List 4A) effective September 1, 2019. Tariffs were delayed on the rest of List 4 (now referred to as List 4B) until December 15, 2019. On August 23, 2019, the Administration announced that List 4A and List 4B tariff rates would increase to 15% upon their effective dates. The President announced via Twitter on September 11, 2019 that the increase would be delayed on List 4A until October 15.

Impacts on Steel & Building Products

It’s been estimated that prior to Section 232 action imports supplied 20 – 40% of U.S. demand for wire rod (raw material for products such as tie wire) and a similar share of the rebar market. The threat of Section 232 action increased the risk of putting import cargoes on the water and the imposition of tariffs made those imports less competitive. Import supply shrunk. Demand previously satisfied by import supply shifted to domestic supply. Basic economics dictate that if supply is restricted and demand is constant, prices will increase. According to American Metal Market indexes, U.S. wire rod prices increased 32% and U.S. rebar prices increased 29% over 2018.

Because Section 232 tariffs left almost all downstream products unprotected, U.S. downstream producers faced rapidly rising raw material costs and competition from imported downstream products unaffected by tariffs. In some cases, imported downstream product prices fell as foreign steel markets were faced with oversupply because of U.S. tariffs. For example, wire rod prices in Beijing declined more than 15% over the course of 2018 according to SteelOrbis indexes. U.S steel prices have since peaked and started to fall as demand has softened at U.S. mills. Downstream producers are now faced with managing high levels of inventory in a declining market.

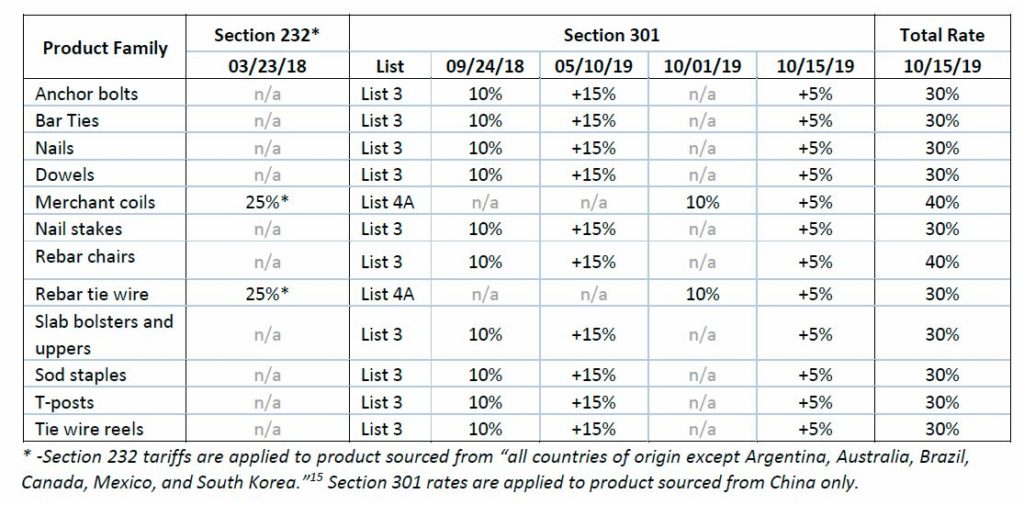

Section 232 tariffs focused on protecting U.S. steel producers and correcting alleged bad behavior in the global steel market. Section 301 tariffs are focused on a much broader range of products and are aimed at correcting a wide range of alleged bad behavior on the part of the Chinese. Steel and building products are only a small portion of the products impacted by Section 301 actions; however, those impacts are significant. MAR-MAC has long offered the line of CONTRACTOR Concrete Construction Products sourced as economically as possible, which frequently means foreign sources – usually China. Section 301 tariffs are driving increased costs in these import products and driving higher costs to our customers. The table below shows the tariff rates impacting CONTRACTOR products according type and effective application and increase dates:

As we’ve navigated tariff-driven volatility in domestic steel and on the import product side of the business, we’ve attempted to insulate our customers from the worst effects. Unfortunately, that’s not always possible and our customers have experienced significant volatility as well. We are working to find alternative sources for these products that will meet quality requirements. Supply chains in a global market are long and change takes time to work through the system.

As always, I’m available to discuss this situation with any of our customers. The situation continues to create a great deal of confusion and uncertainty and we very much appreciate our customers’ understanding and patience. If you’d like to discuss the situation further, you can reach me at 843-335-6718 or jarrett.martin@marmacinc.com.

Sources